Re-Lending

- If you supply an underlying asset, it is first deposited into Aave to generate an aToken, which is then re-lent to 246 Club.

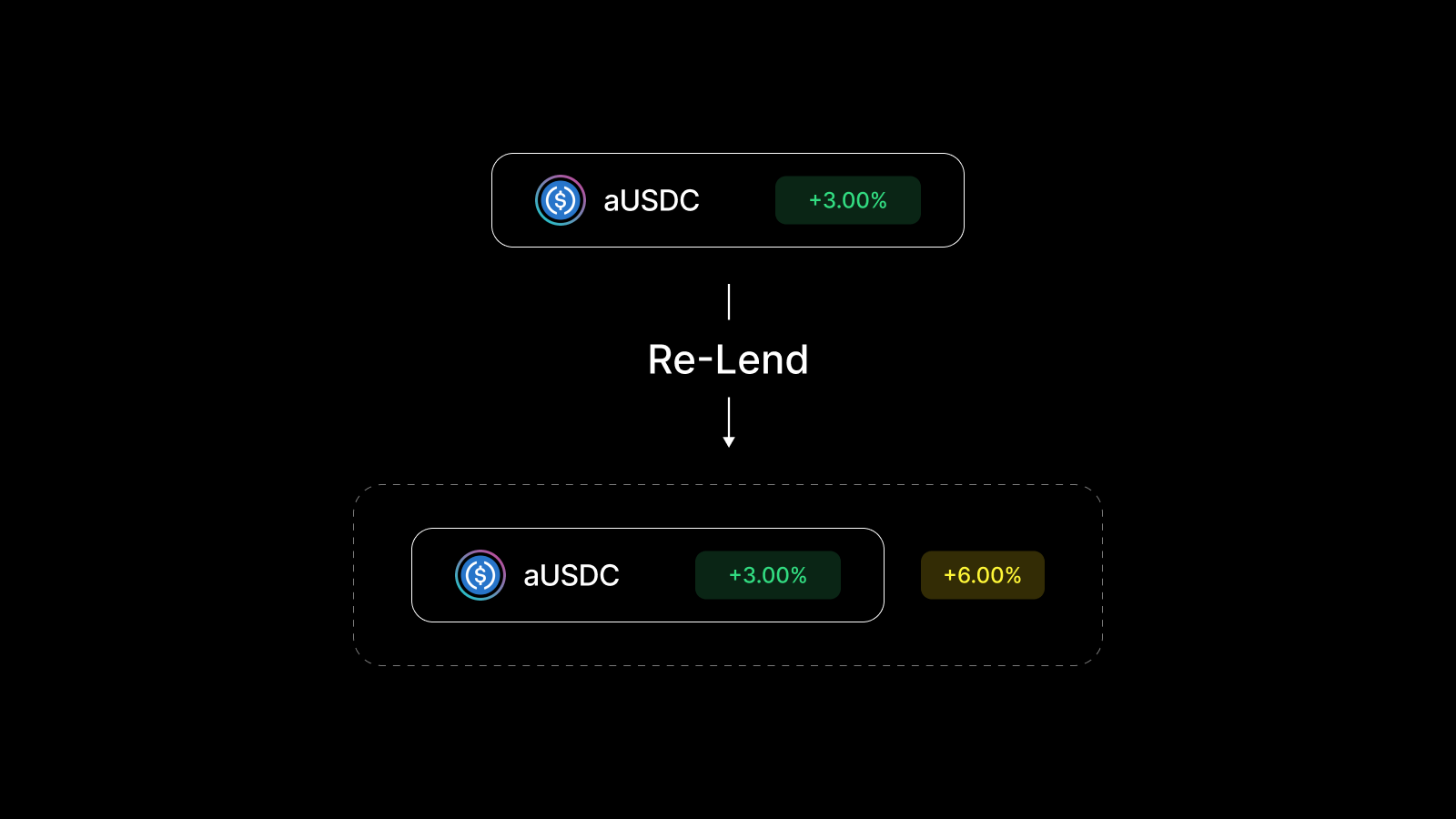

- If you supply an aToken directly, it is re-lent to 246 Club.

- When you lend to Aave (e.g., 100 USDC), you receive an aToken as a receipt of your deposit (e.g., 100 aUSDC) and gain borrowing power based on Aave’s LTV ratio. For example, with an 80% LTV, you can borrow up to 80 USDC.

- By re-lending your aToken (e.g., 100 aUSDC) to 246 Club, you delegate this borrowing power( e.g., 80USDC in this case ) to the protocol.

- Arbitrageurs on 246 Club utilize this borrowing power and pay additional interest (see Interest Rate Model), which generates the extra yield for your Re-Lending position.

Note on Arbitrageurs: In 246 Club, arbitrageurs are active participants who borrow funds to execute cross-protocol strategies. While they function as borrowers in the system’s loan mechanics, we use the term ‘arbitrageur’ to emphasize their role in identifying and capitalizing on market inefficiencies between different markets.

You cannot borrow against a re-lending position from 246 Club.

Cross-Protocol Arbitrage

- Arbitrageurs deposit assets into a Morpho Vault and borrow assets against it from Aave.

- If they don’t have an existing Morpho position, 246 Club’s user interface allows them to “zap” into a Morpho Vault position and immediately borrow against it from Aave.

- This setup enables interest rate arbitrage between yield from Morpho deposits and borrowing rates from Aave.

- Once established, the leveraged arbitrage position must be maintained to ensure a healthy loan-to-value ratio, similar to looping from other lending markets. (see the Managing Arbitrage Position page for details)