Design Principle

Interest Rate Model in the 246 Club is designed to intersect between two primary objectives.- Unified Liquidity

- Market-based large unified liquidity pool.

- Pair Specific Sensitivity

- Interest rate sensitively reflects the pair-specific borrow demand.

246 Rate on top of Aave Rate

As a Re-Lending protocol, the Interest rate in the 246 Club applied to Re-Lenders and arbitrageurs differs from conventional lending protocols. For Arbitrageurs : On top of the Aave borrow rate, arbitrageurs are charged with the 246 rate.Aave borrow rate serves as a baseline borrow rate

Pair Specific Interest Rate

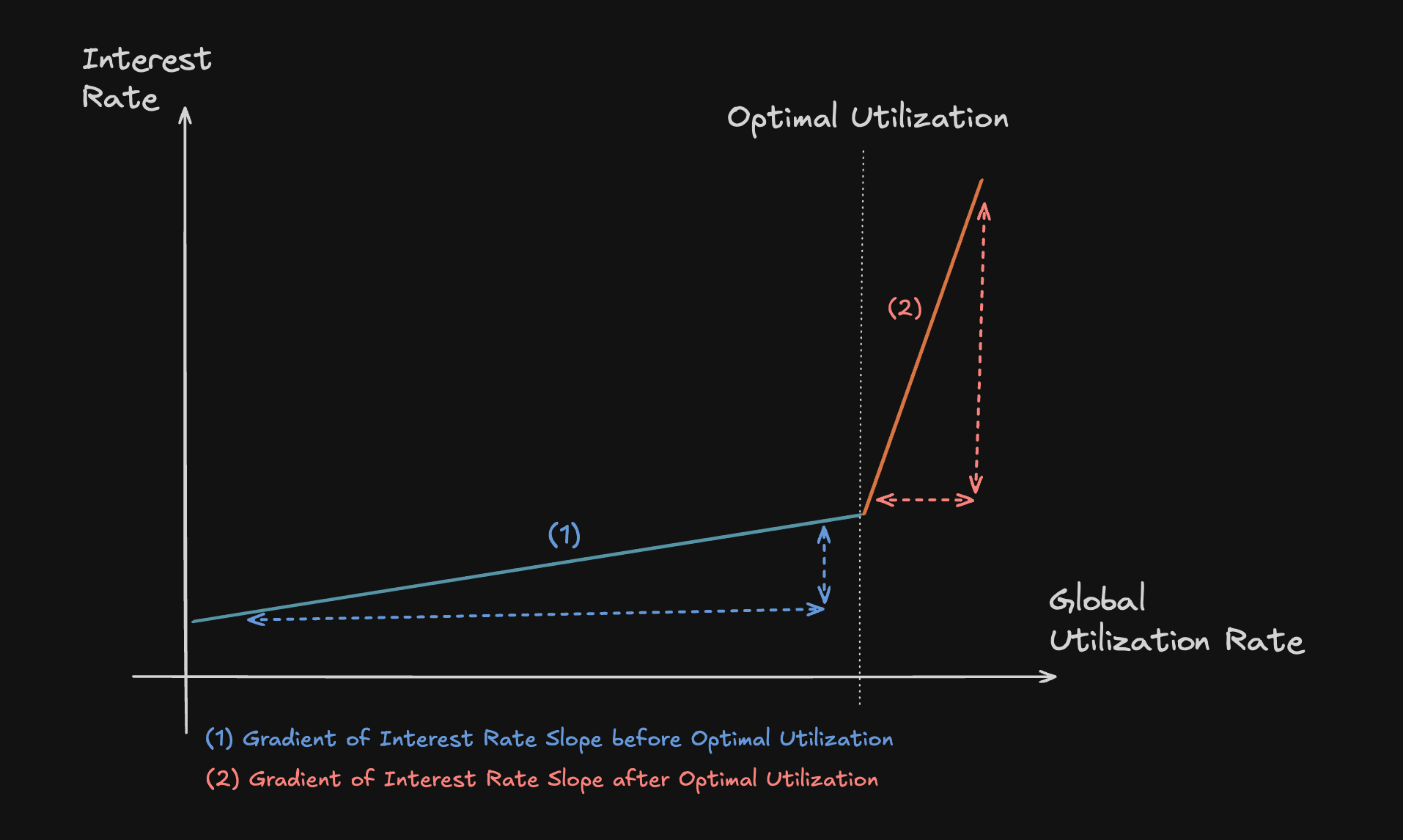

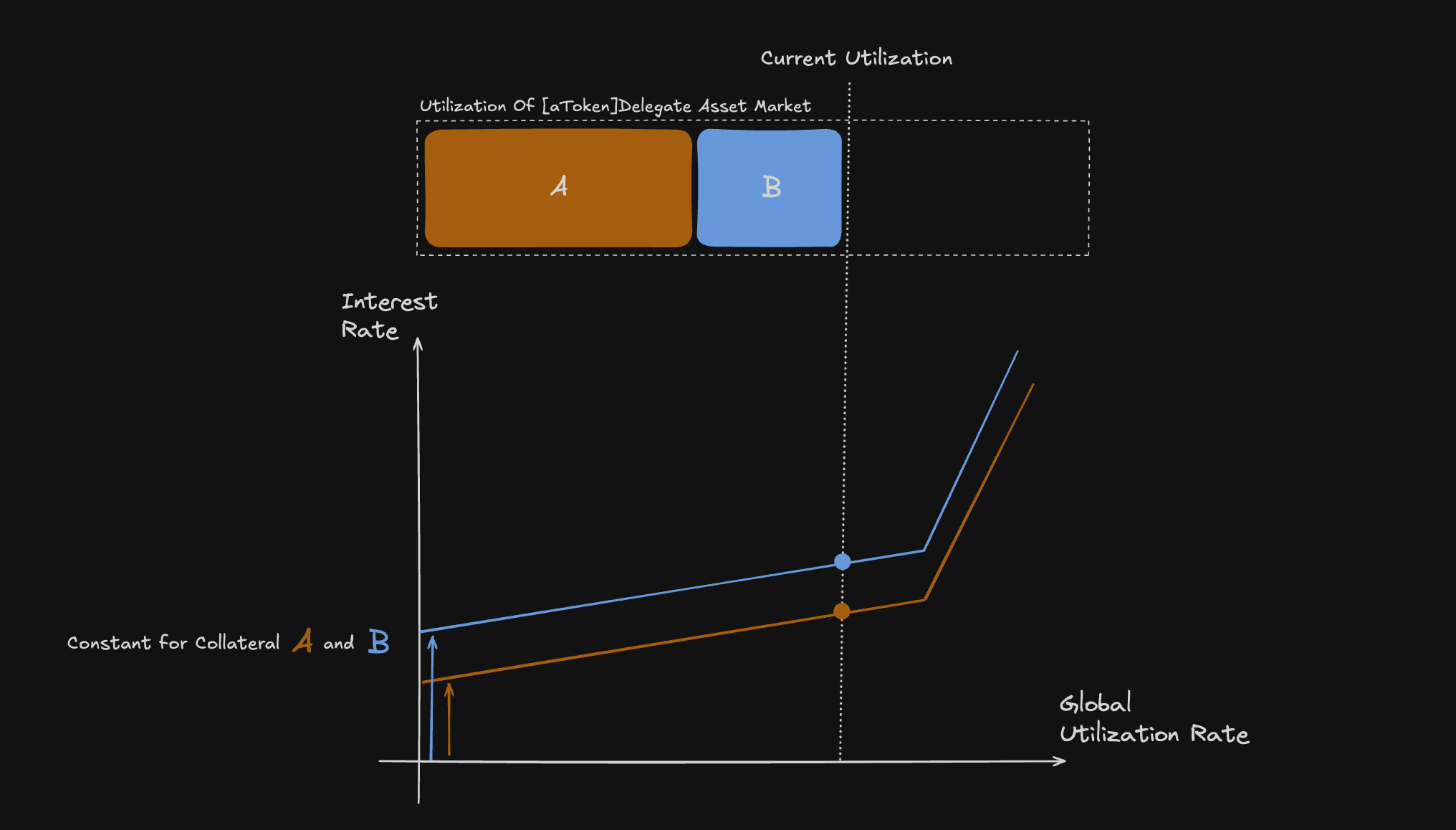

Each unified pool of each Market consists of a single borrow asset and multiple different collateral*. Regardless of the number of collateral assets against which the borrow asset is exposed, as a unified pool, utilization is calculated by the total borrowed over the total borrowing power delegated in this market.*More details on Market StructureFor example, in the [aUSDC]USDC Market, the total supply of delegated USDC is 100. Various arbitrageurs have borrowed 20 USDC against Collateral A and 40 USDC against Collateral B. Regardless of the composition of each pair, utilization is calculated by the total borrowed, 60 USDC, over the total borrowing power delegated, 100 USDC, which is 60%. Each pool regulates supply and demand dynamics based on this global utilization. Therefore, interest rates specific to each pair, within a single market, will have the same interest rate gradient and therefore experience the same rate of change in interest rate as well as optimal utilization.

Gauging Pair-Specific Demand via Buffer Allocation

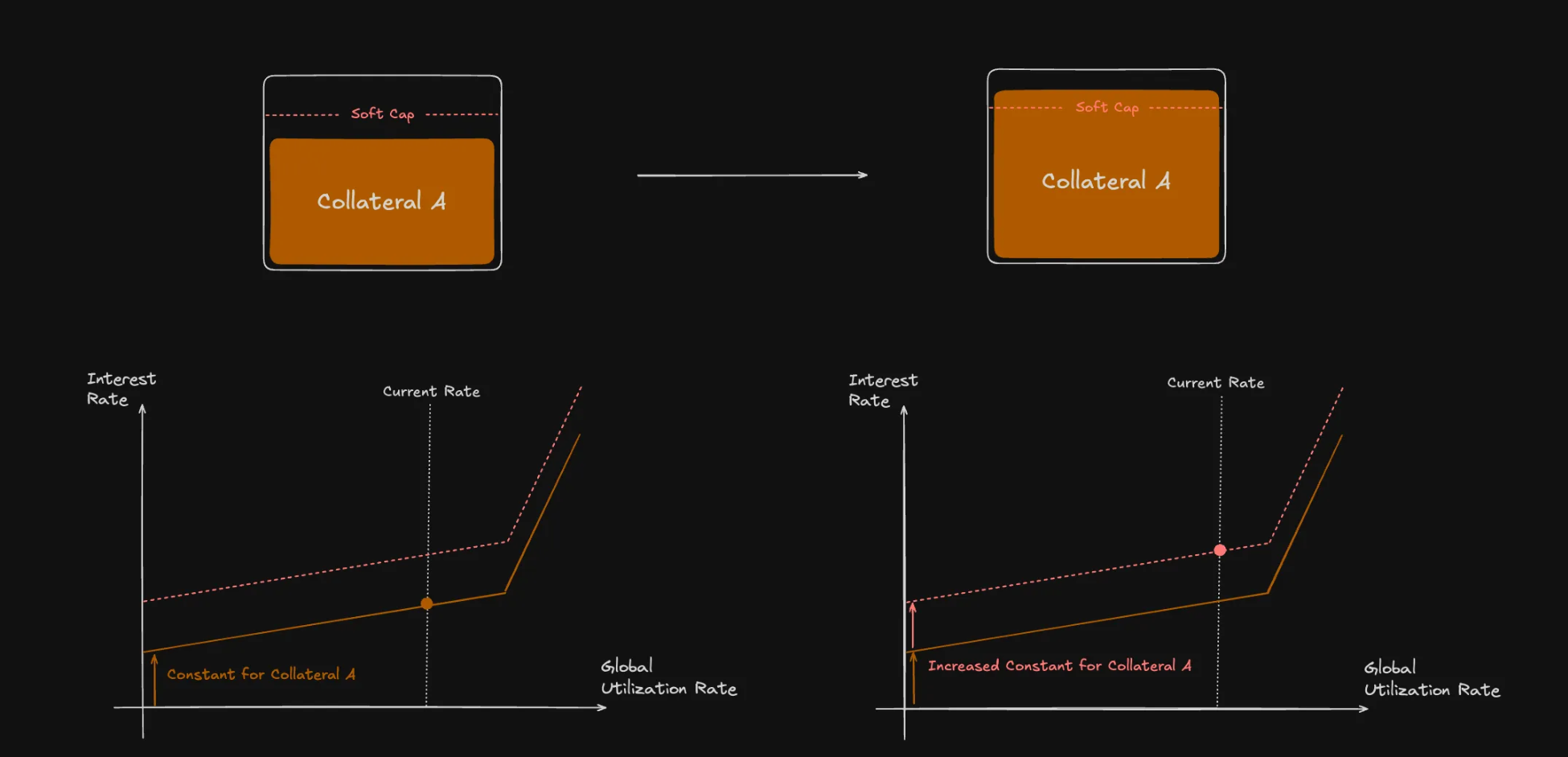

Among the two types of caps(Hard and Soft) mentioned on the previous page, Segmented Risk Exposure, Hard Cap represents the maximum borrow limit of that pair; once the Hard Cap is tapped, no more borrowing is permitted. On the other hand, Soft cap is not a hard restriction on borrowing capacity but rather a gauge of the demand specific to each pair. Pairs not only have their own interest rate curve but are also dynamic in reacting to the demand specific to each pair. Once the borrowing demand of the pair touches the predetermined Soft Cap, this indicates heightened borrow demand. And so the pair-specific constant shifts upwards.

Example

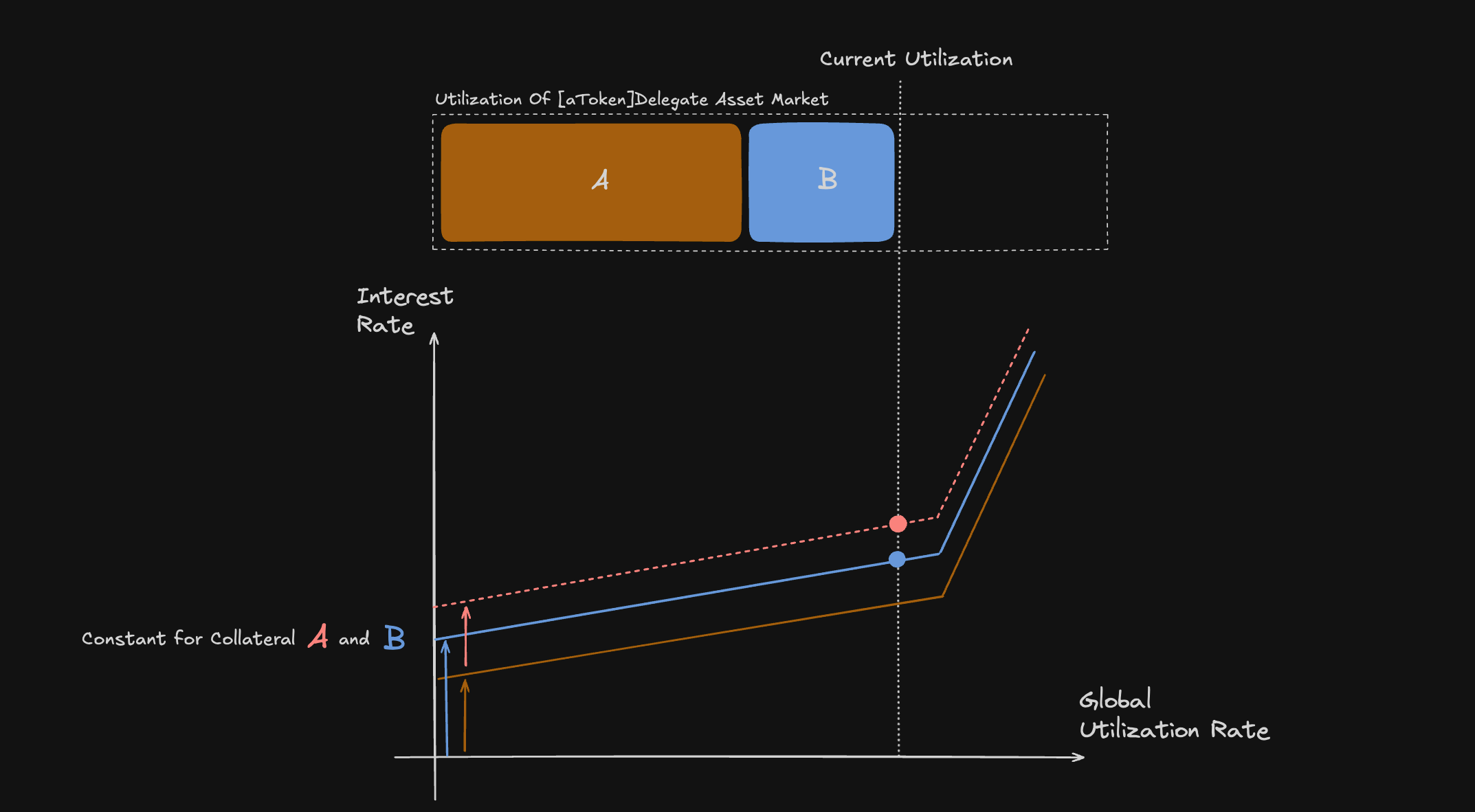

Consider [aUSDC]USDC market exposed to Collateral A and B within the same unified pool, both with a defined Soft Cap.- Increased borrow demand of Collateral A With more arbitrageurs now borrowing against Collateral A, the Soft Cap of Collateral A has been surpassed.

- Collateral A under Buffer Allocation Reserved Buffer is allocated to Collateral A, and arbitrageurs pay Buffer Premium on top of Base Rate(Aave Rate + 246 Rate) to further borrow with Collateral A.

- Rate of Collateral B Meanwhile, the rate of Collateral B remains mostly unaffected, as Collateral B has not reached its Soft cap.