Risk of Aave

At 246 Club, we build our Re-Lending on Aave, a leading DeFi lending protocol with a strong history of security and resilience across multiple blockchain networks. While Aave’s proven track record gives us a solid foundation, our Re-Lending mechanism—using Aave positions like aUSDC as underlying assets—introduces specific risks. Here’s how we manage Aave-related risks to keep our markets stable. Our primary exposure comes from the lending positions on Aave, such as aUSDC, that re-lenders use in markets like [aUSDC]USDC. If bad debt (unrepayable loans) occurs in the aUSDC pool, it could affect your relent position. For example, if you re-lend 100 aUSDC, bad debt on Aave might impact the stability of that position in our market. However, with Aave’s Optimistic Accounting, Aave delays the impact of bad debt on aTokens like aUSDC. If bad debt occurs, your 100 aUSDC won’t lose value immediately, giving us time to address the issue. Also, Aave’s Umbrella feature will prevent small bad debt from accumulating and absorb any residual debt, further protecting your relent position. For a deeper understanding, check Aave’s risk documentation on market volatility, smart contracts, and liquidations: Aave Risk Documentation.Liquidity Risk

In Re-Lending, liquidity risk arises when the demand for borrowing exceeds the available borrowing power, potentially limiting withdrawals from the pool. At 246 Club, we manage this risk carefully by monitoring the utilization ratio of each market and using mechanisms to balance supply and demand. Let’s break this down to understand how we calculate utilization, what it means for withdrawals, and how we ensure stability in our markets, like the [aUSDC]USDC market. Utilization Ratio in Re-Lending Market The utilization ratio in a Re-Lending market tells us how much of the delegated borrowing power is being used. It’s calculated as:Utilization Ratio = Borrowing Power Used / Total Delegated Borrowing Power

Let’s take the [aUSDC]USDC market as an example. Suppose a re-lender deposits 100 USDC on Aave, which becomes 100 aUSDC (Aave’s token for deposited USDC). From this, they delegate borrowing power worth 80 USDC to the protocol. If arbitrageurs use 72 USDC of that borrowing power, the utilization ratio is:

72 USDC (borrowed) / 80 USDC (delegated borrowing power) = 90%

This 90% utilization ratio means that 90% of the available borrowing power in the [aUSDC]USDC market is in use. The remaining 10% is what we call the underutilized portion, which plays a key role in managing liquidity and withdrawals.

Withdrawals

In the [aUSDC]USDC market example, with a 90% utilization ratio, the remaining 10% of the delegated borrowing power is underutilized. This underutilized portion determines how much can be withdrawn from the total re-lent amount. Since the re-lender has 100 aUSDC in the market, the withdrawable amount is:

100 aUSDC x 10% (underutilized portion) = 10 aUSDC

This means that, at 90% utilization, only 10 aUSDC can be withdrawn from the market at that moment. The rest of the aUSDC is tied up supporting the 72 USDC that arbitrageurs have already utilized, ensuring the market remains stable for all participants.

High Utilization and Liquidity Risk

Liquidity risk becomes a concern when utilization gets extremely high—say, 95% or more. In such cases, the underutilized portion shrinks, meaning less can be withdrawn. For example, if utilization in the [aUSDC]USDC market rises to 98%, only 2% of the delegated borrowing power is underutilized, so the withdrawable amount becomes:

100 aUSDC x 2% = 2 aUSDC

This limited withdrawal capacity is a natural part of pool-based systems during high demand. It ensures that the market maintains sufficient liquidity, protecting both re-lenders and the protocol.

The 246 Interest Rate Curve

The 246 Interest Rate Curve adjusts interest rates based on the utilization ratio. In pool-based lending models, interest rates often follow a curve where rates increase as utilization rises. For example, a typical model might set a low borrow rate (e.g., 2%) at 0% utilization, but as utilization approaches 100%, the rate could jump to 20% or higher. This encourages arbitrageurs to repay loans (reducing utilization) and attracts more re-lenders to deposit (increasing available borrowing power).

At 246 Club, our Interest Rate Curve works similarly. If the [aUSDC]USDC market hits 90% utilization, the curve might increase the borrow rate for USDC, making borrowing more expensive. This discourages new borrowing and encourages arbitrageurs to repay their loans, lowering utilization. At the same time, higher utilization could increase the yield for re-lenders, incentivizing more aUSDC deposits, which adds more borrowing power to the market. These adjustments help the market return to a normal utilization level, like 70–80%, where withdrawals are easier and liquidity is more balanced.

Collateral Risk

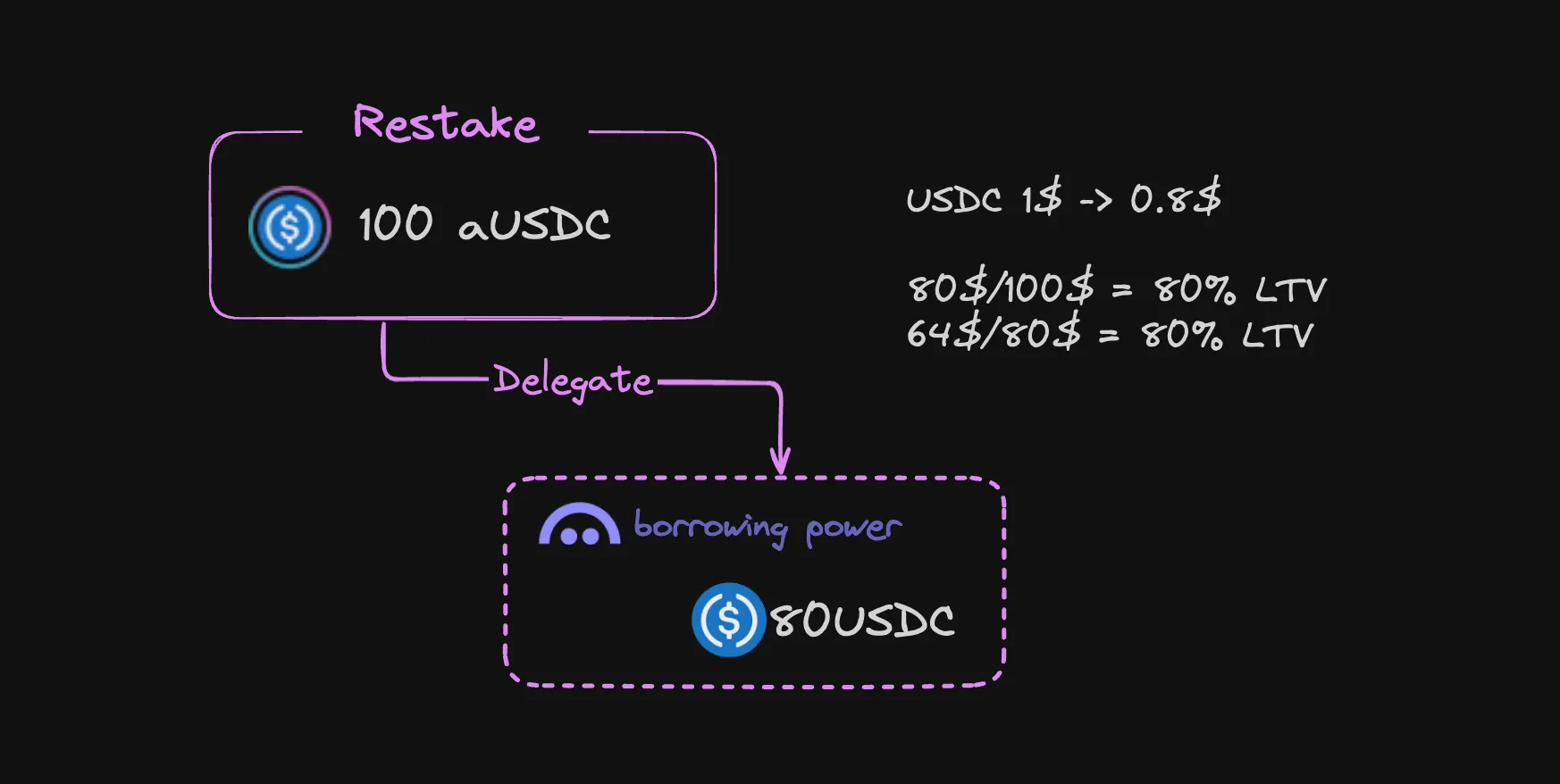

In Re-Lending at 246 Club, re-lenders lend assets on Aave (like aUSDC) against Aave’s collaterals while also lending their borrowing power against different collaterals on 246 Club. Collateral risk arises when the value of assets used as collateral drops, leading to undercollateralization or bad debt. For example, if you re-lend 100 aUSDC on Aave, its value supports borrowing power delegated to our [aUSDC]USDC market. If the collateral on Aave (like aUSDC) or on 246 Club (like an arbitrageur’s collateral) loses value, the position’s health can decrease. If bad debt (unrepayable loans) builds up in these lending positions, it could impact the stability of your re-lent positions. At 246 Club, we mitigate collateral risk to keep your re-lent positions stable by using careful strategies: we set Loan-to-Value (LTV) ratios, like allowing only 80 USDC of borrowing power from 100 Morpho USDC position (80% LTV), creating a buffer against collateral value drops that we adjust as market conditions change; we employ liquidation mechanisms to protect the market, partially liquidating undercollateralized positions on 246 Club to repay debt if collateral values fall too low ( Details on Liquidation Mechanism can be found here ); and we use Segmented Risk Exposure (SRE) to limit risk by dividing our single liquidity pool into segments with caps for each collateral, pausing borrowing if a collateral in the [aUSDC]USDC market hits its 10% cap to shield the pool ( More Details ).Re-Lending for existing Borrowers of Aave

If you’re currently borrowing on Aave, you might be curious about how Re-Lending with 246 Club works alongside your existing loan. Suppose you have 100 aUSDT on Aave, backing a 20 DAI loan. You don’t need to move your entire position to 246 Club. With Re-Lending, you can re-lend just a portion of your aUSDT to earn extra yield while keeping your Aave loan safe. Here’s how it works:- If you re-lend 20 aUSDT out of your 100 aUSDT, you’ll have 80 aUSDT left on Aave.

- This 80 aUSDT continues to support your 20 DAI loan.

- Your Loan-to-Value (LTV) ratio adjusts from 20% to 25% (20/80).

Risk Specific to Credit Delegation

1) The Dual-Position Structure in Re-Lending

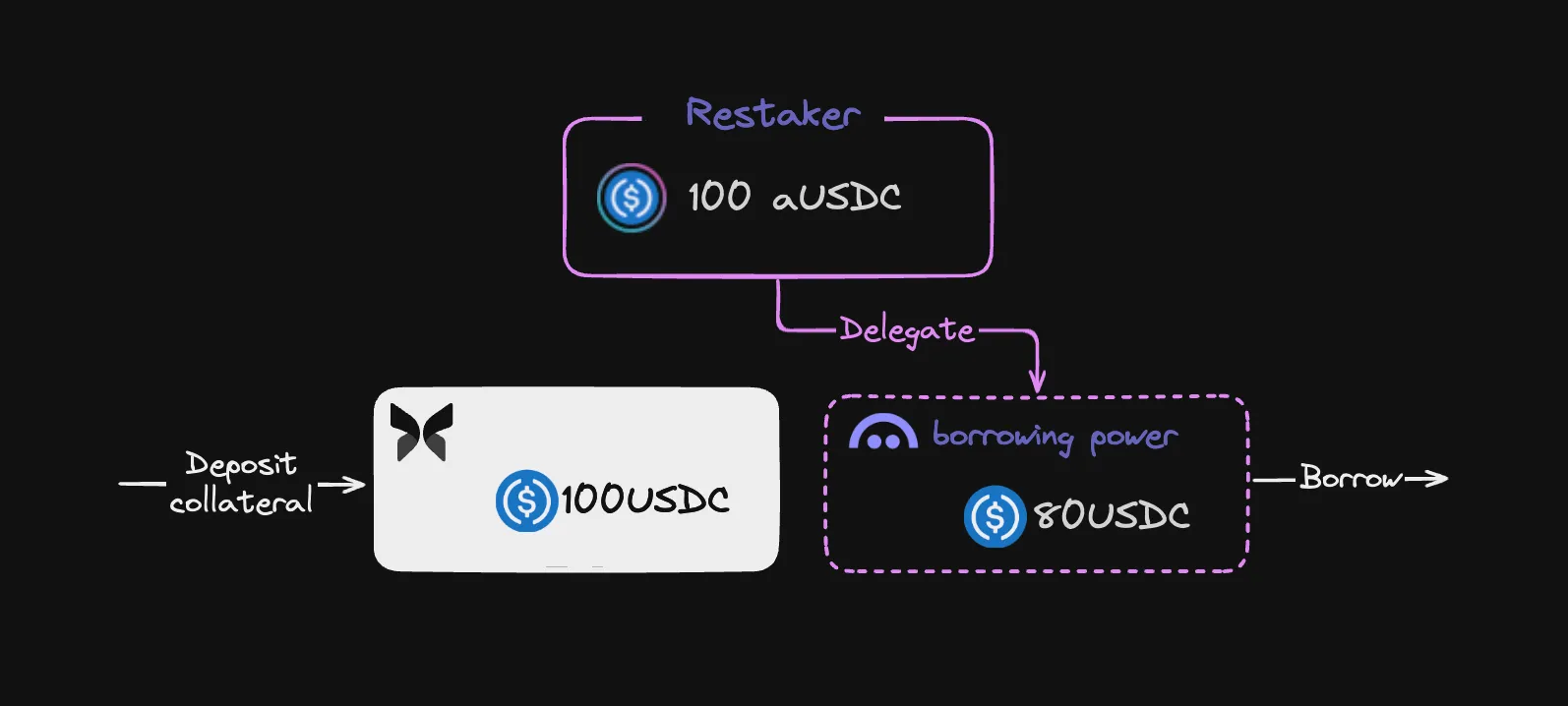

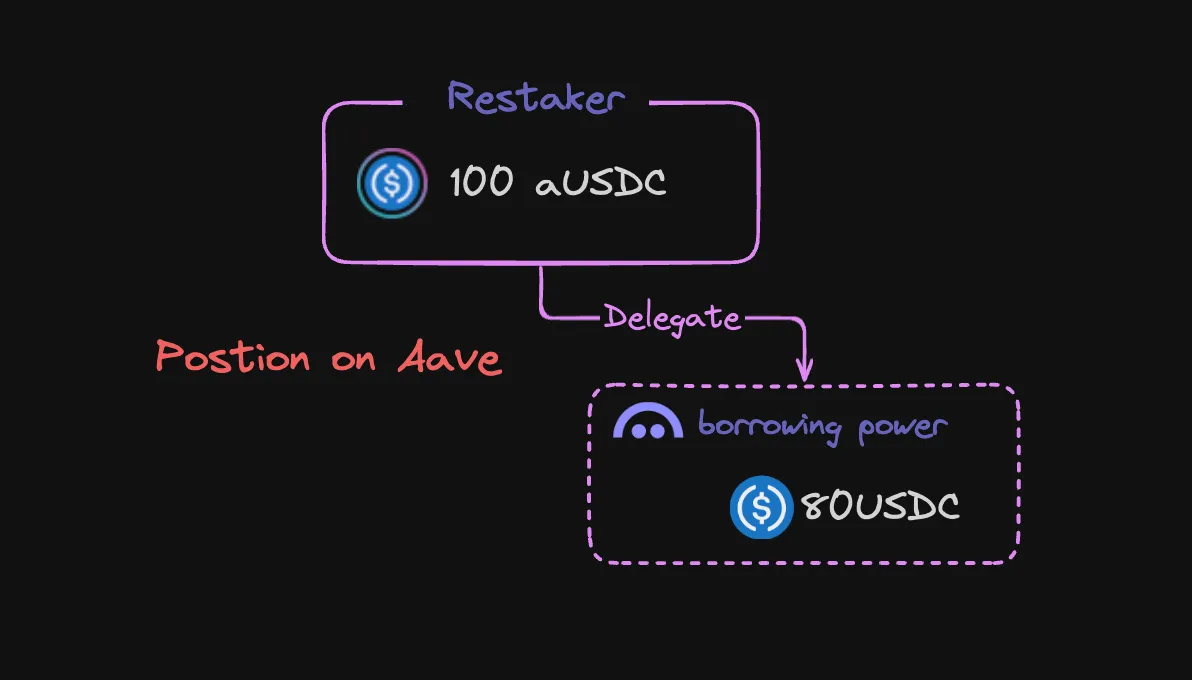

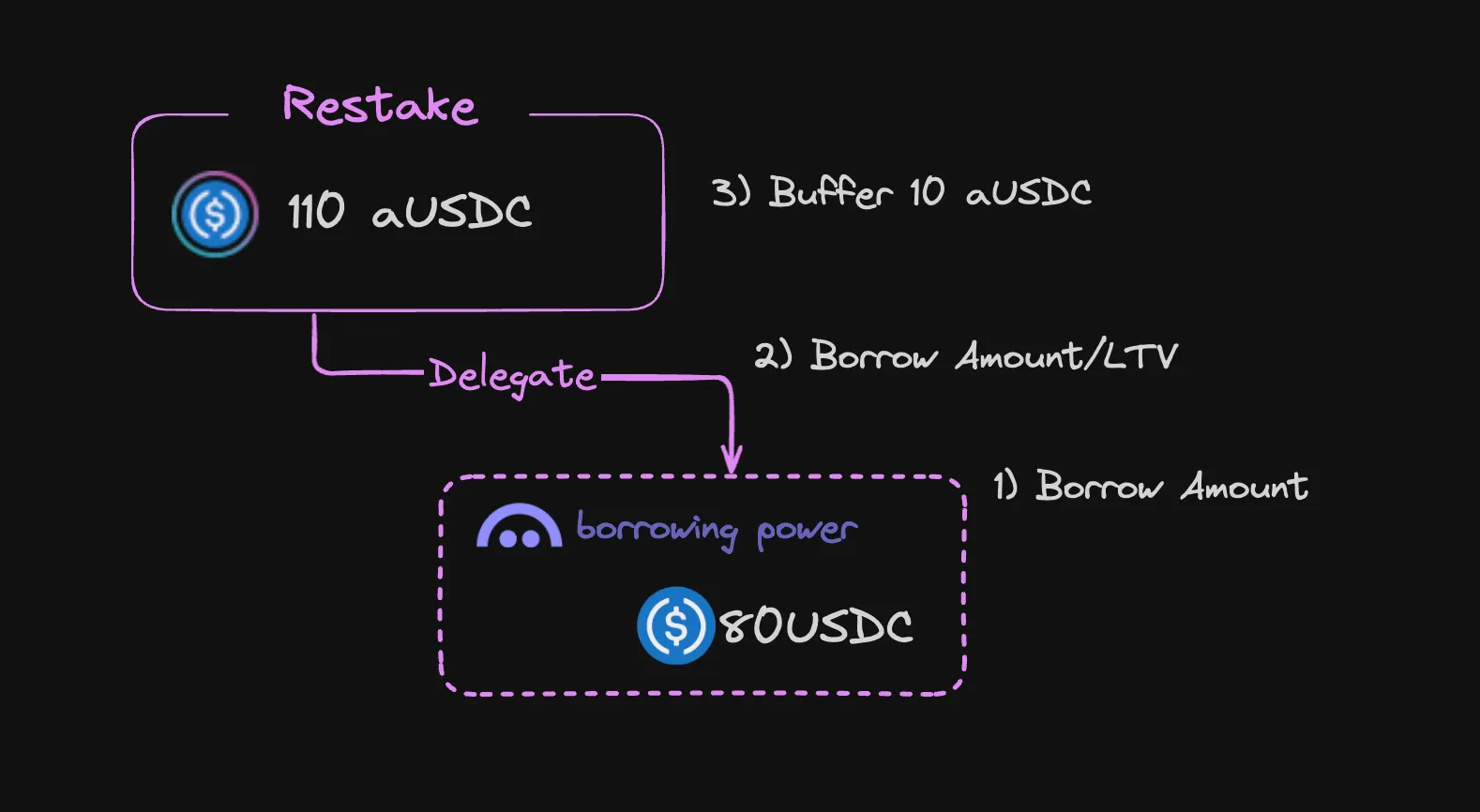

When an arbitrageur opens a loan position through 246 Club, two distinct positions are created:- Aave Position: This involves the re-lender’s activity. A re-lender deposits assets (e.g., 100 USDC, which becomes 100 aUSDC on Aave) and delegates borrowing power (e.g., 80 USDC) to the protocol.

- 246 Club Position: This is the arbitrageur’s cross-protocol position. The arbitrageur deposits collateral (e.g., 100 USDC on Morpho, a lending protocol integrated with 246 Club) and borrows 80 USDC using the delegated borrowing power from the re-lender.

- Re-Lender’s Flow (Purple): The re-lender re-lends 100 aUSDC on Aave and delegates borrowing power equivalent to 80 USDC.

- Arbitrageur’s Flow (White): The arbitrageur deposits 100 USDC as collateral on Morpho and borrows 80 USDC from Aave using the delegated borrowing power.

- Collateral: 100 aUSDC (representing the 100 USDC deposited by the re-lender).

- Debt: 80 USDC borrowed from Aave using the delegated borrowing power.

- Collateral: 100 USDC deposited on Morpho.

- Debt: 80 USDC borrowed, utilizing the delegated borrowing power from the re-lender.

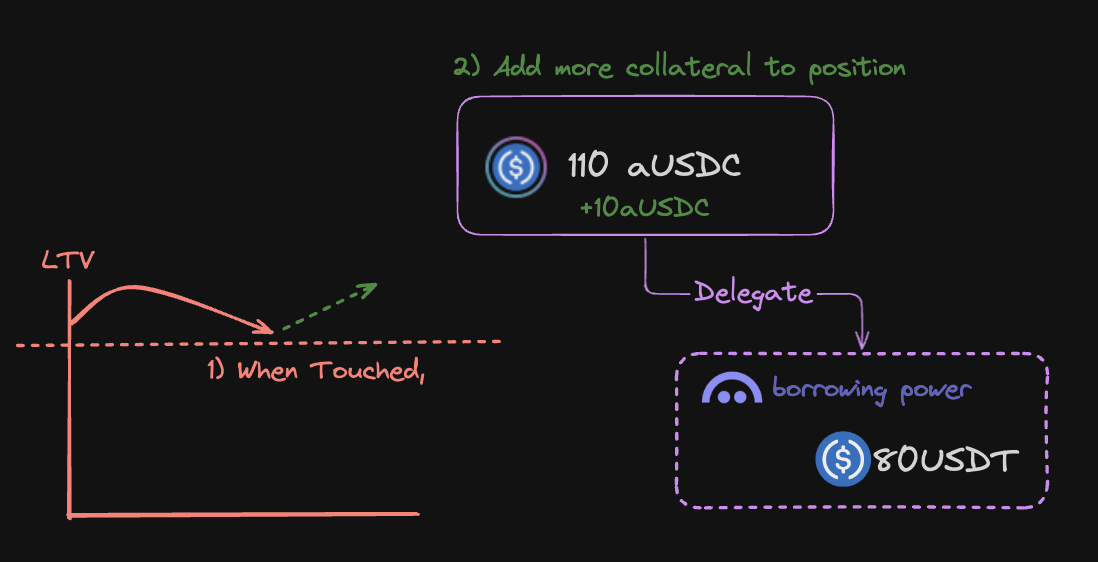

2) Risk Management for the Aave Position

To mitigate the risk of liquidation on the Aave position, 246 Club employs several strategies, ensuring stability even in adverse market conditions. 1. Matching Re-Lending and Delegation Assets

- A primary bot connected to multiple nodes.

- A secondary bot as a backup.

- Manual intervention by the 246 Club team or users.

3) Extreme Scenarios for Liquidation

Liquidation on the Aave position would only occur under highly unlikely conditions:- Rapid Interest Rate Spikes: Interest rates accelerate toward the LTV limit, overwhelming the buffer, while both primary and secondary bots (and manual intervention) fail to trigger adjustDelegation.

- Major Stablecoin Depegging: A swift depegging of stablecoins pushes the position past the buffer, with bots and manual intervention failing to act in time.

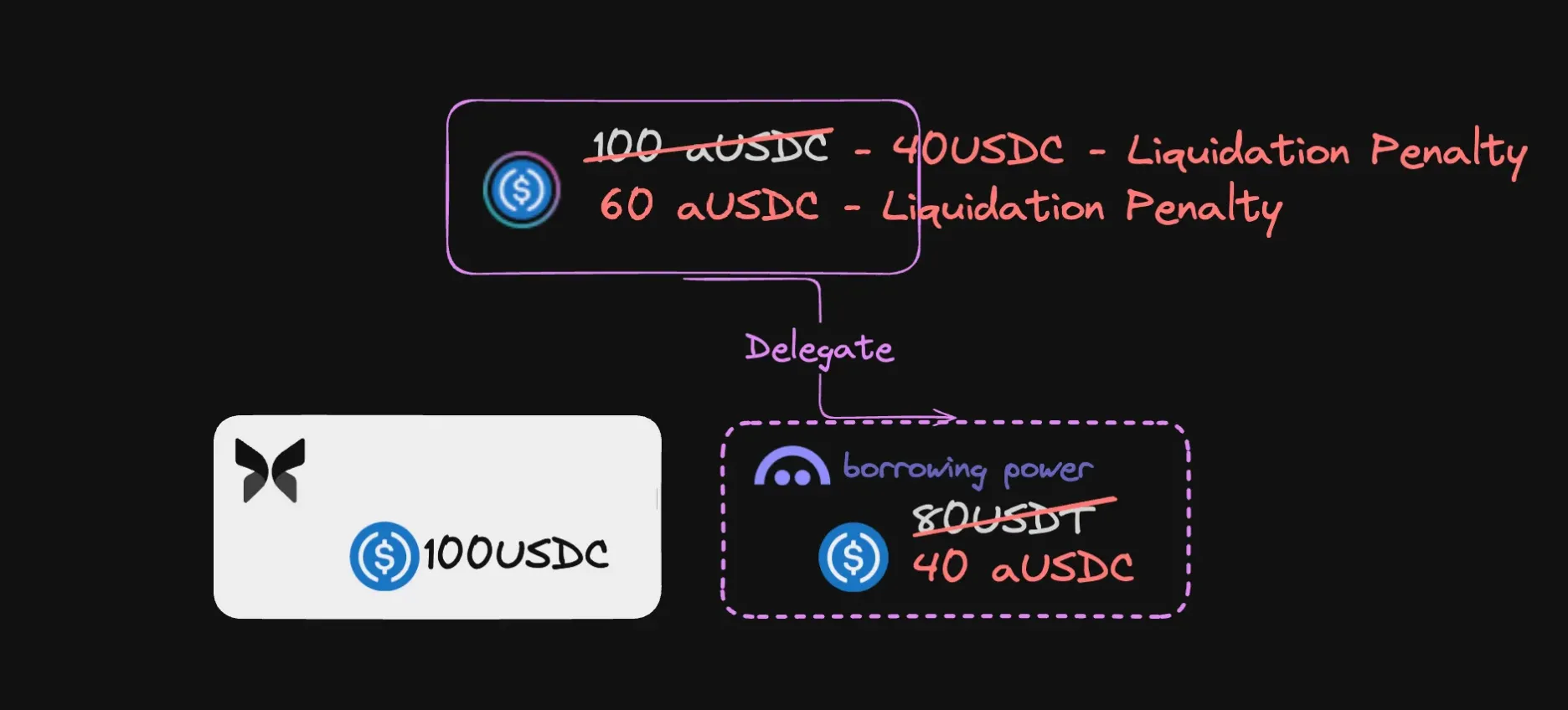

4) What Happens If Liquidation Occurs?

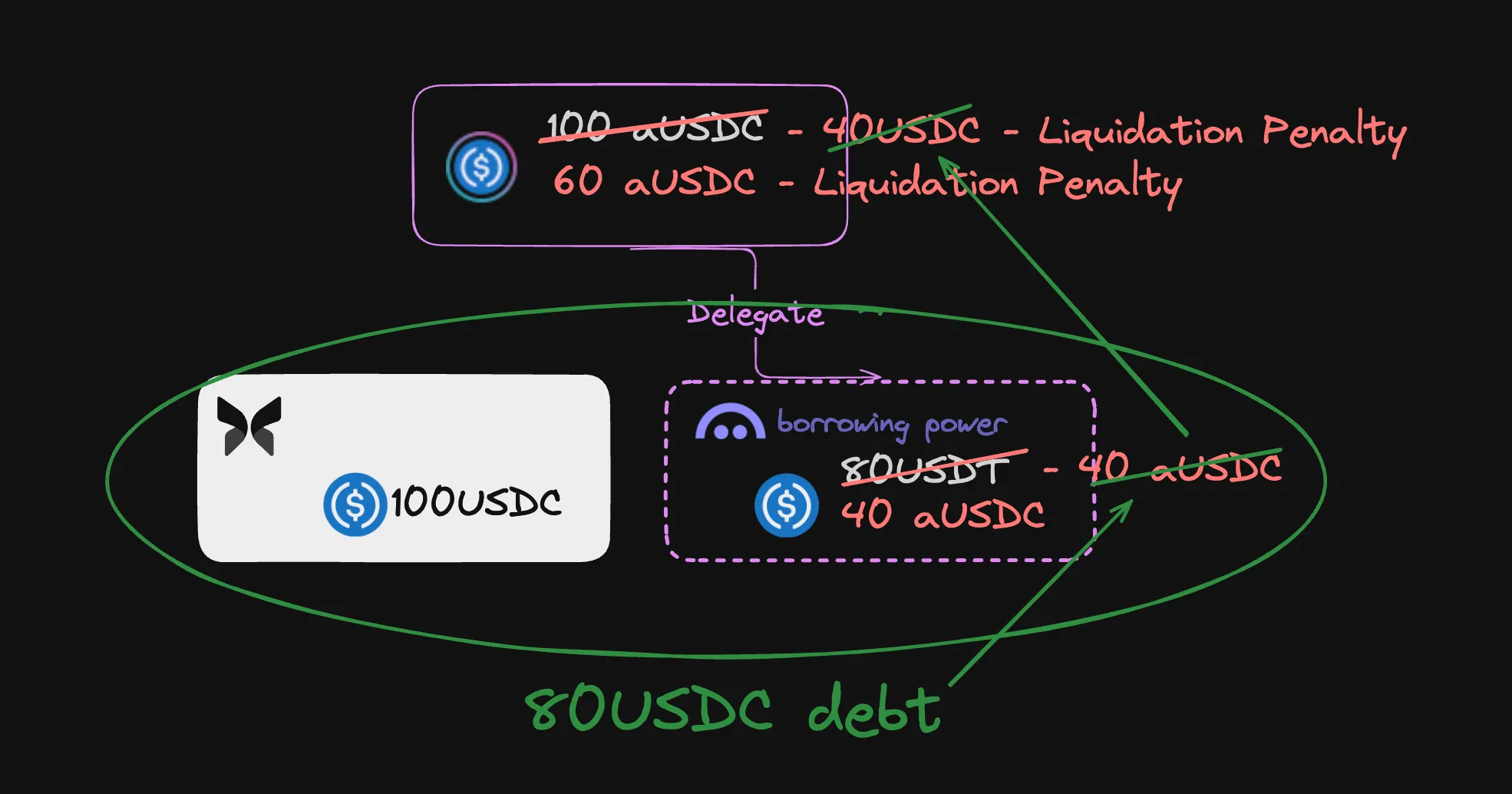

Despite these safeguards, liquidation on the Aave position is still possible in extreme scenarios. Let’s explore what happens if liquidation occurs, considering Aave’s close factor of 50% (meaning 50% of the position is liquidated to repay debt). Liquidation on Aave If the Aave position is liquidated:- Collateral: 100 aUSDC is reduced to 60 aUSDC (after a liquidation penalty).

- Debt: 80 USDC is reduced to 40 USDC (50% repaid during liquidation).

- The 80 USDC repayment covers the remaining 40 USDC debt on Aave.

- The remaining 40 USDC (after securing 60 aUSDC worth of collateral on Aave) is returned to the pool.