Why Segmented Risk Exposure?

The Isolated vs. Unified Dilemma

- Unified Pools

- Upside: A single large reservoir where depositors earn yield from the entire market. Borrowers freely access liquidity with minimal friction.

- Downside: All participants are tied to every collateral’s performance; a risky or highly demanded collateral can dominate the entire pool.

- Isolated (Pair-Based) Pools

- Upside: Lenders and borrowers know precisely which collateral(s) they’re exposed to. Each market stands on its own, preventing risk contagion.

- Downside: Liquidity becomes scattered across many small pools. This fragmentation can lead to inefficient interest rates, as each isolated pool juggles supply and demand on its own.

How SRE Works

One Large Pool, Multiple Segments

Under SRE, all capital (supplied by re-lenders) resides in a single pool—no need to split up your deposits across multiple mini-markets. However, this big pool is internally divided into “segments,” each allocated to a specific collateral.- Segment Caps Each collateral gets a maximum borrowing limit within the overall pool. Once a collateral hits its cap, borrowing capacity for that collateral is effectively “paused,” protecting the rest of the pool from unlimited exposure.

- Collateral-Specific Settings We can fine-tune how aggressively or conservatively each collateral can draw from the pool. Some collaterals have strict caps (a hard limit), while others use soft caps (a limit that can dynamically adjust under certain conditions).

- On-Demand Liquidity As long as a collateral hasn’t reached its limit, borrowers tap into a common liquidity source. This is more flexible than purely isolated markets and typically allows for more stable borrowing and lending rates (see the Interest Rate Model for how rates are calculated).

Example Scenario

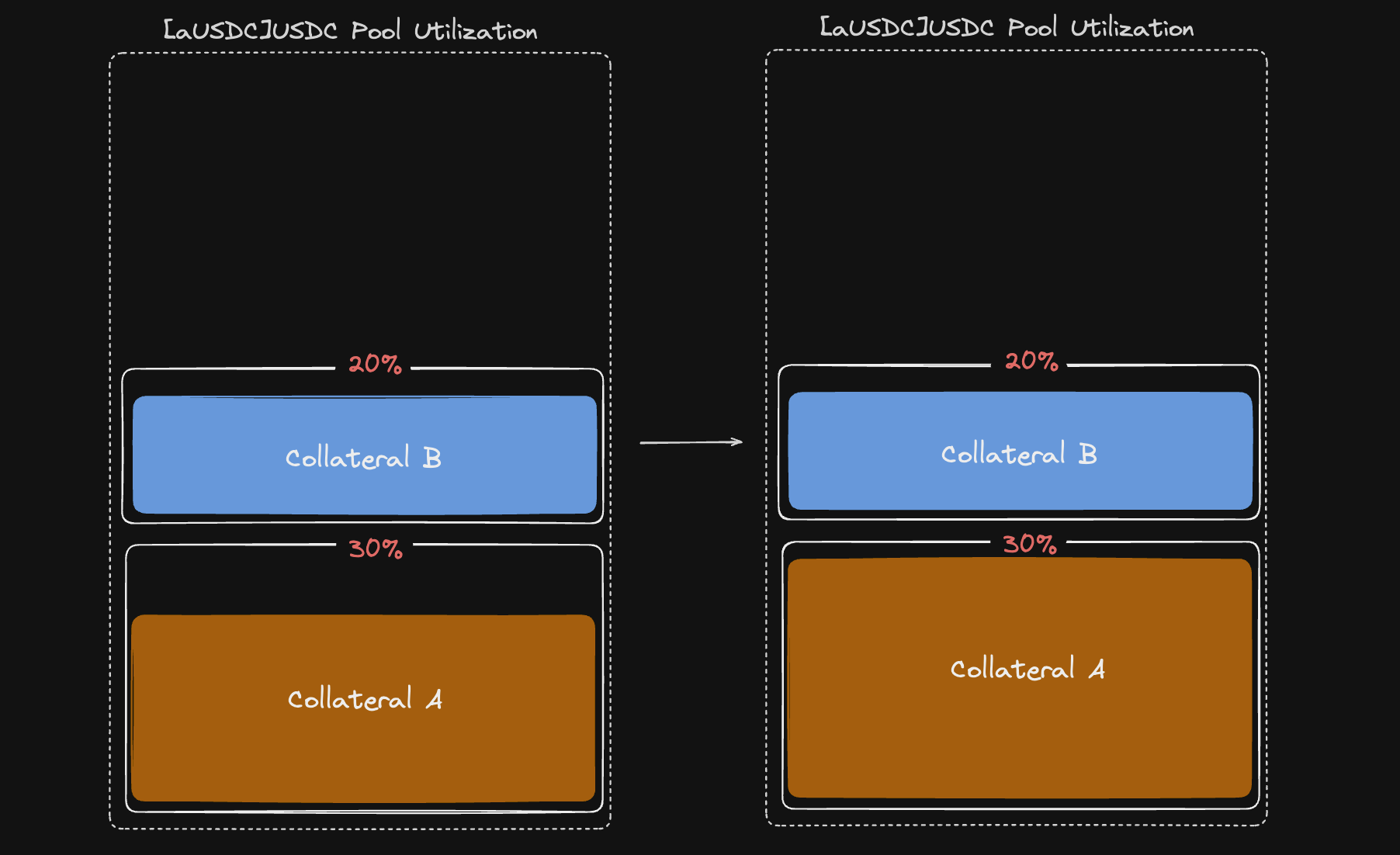

- You deposit aUSDC into [aUSDC]USDC market. All borrowing power delegated to this market shares liquidity.

- Collateral A listed in this market can borrow up to, say, 30% of the pool’s total capacity, while Collateral B might have a separate 20% allocation.

- If Collateral A’s demand is sky-high and it nears its 10% cap, further borrowing for A gradually tightens or halts—without impacting B’s share, which remains open as long as B’s own segment has capacity.

Benefits and Implications of SRE

(A) Reduced Fragmentation, Preserved Liquidity With SRE, lenders don’t have to manually chase yields across dozens of isolated pools. They deposit once into one reservoir. Borrowers still benefit from a larger overall liquidity base, meaning fewer “empty” or underutilized markets. (B) Targeted Risk Control By capping each collateral’s draw, we limit how much it can influence the pool. If a new or potentially volatile collateral sees a surge in borrowing demand, it can’t swallow the entire supply. That effectively shields lenders from unlimited exposure to any single risk factor. (C) Flexibility with Caps Soft caps let us react to real-world conditions:- If a collateral proves safe and popular, we can raise its cap.

- If it starts to show signs of excessive volatility, we keep its cap low or revert to a hard cap.

- Cap Overshoot: If a cap is set too low, demand goes unmet even if the larger pool has free liquidity.

- Governance Updates: SRE requires active monitoring. Caps may need tweaking as market conditions shift.

- Not as Isolated as Pure Silo: Although SRE segments risk, it’s not a complete silo model—collaterals still share an overarching pool.